In a new report, Yole Group provides a global overview of the semiconductor device industry in numbers while also covering semiconductor device technology and market trends.

Market Growth and Global Demand Fuel the Semiconductor Device Industry

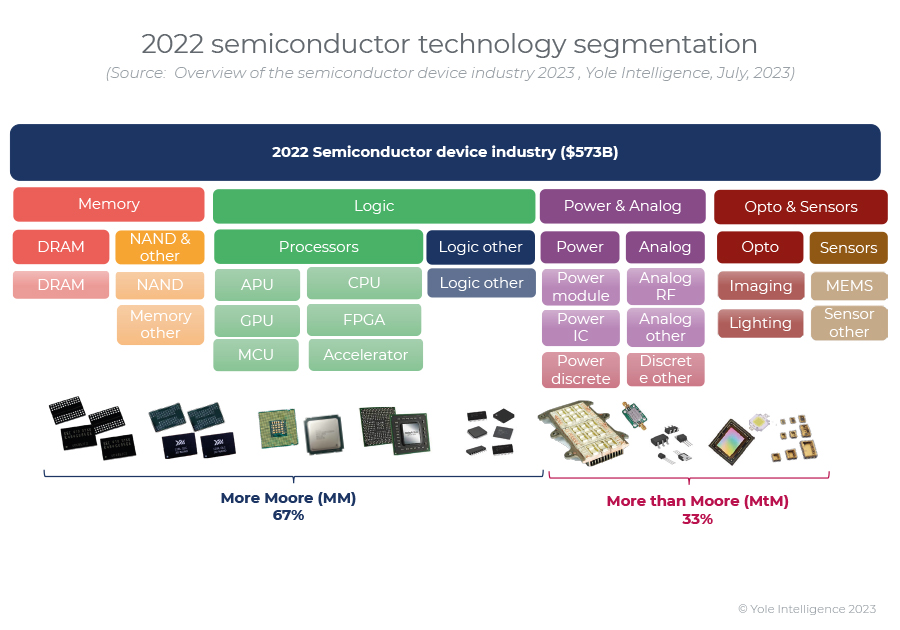

Semiconductor device revenue peaked in 2022 at $573 billion and is expected to retreat 7% to $534 billion in 2023. This industry plays a critical role in enabling technological advancements across various sectors, including mobile & consumer, infrastructure, automotive, industrial, and more. Over the past few decades, the industry has experienced a sustained 6.4% CAGR, driven by increasing demand for mobile & consumer electronics, the rise of internet applications such as social media, and the rapid digitalization of most industries.

Integrated circuits are becoming smaller, more powerful, and capable of handling complex tasks, paving the way for new technology advancements such as artificial intelligence, machine learning, and edge computing. This evolution presents both opportunities and challenges for companies in the industry, requiring them to invest massively in R&D and capital expenditure for new foundries to maintain significance in this fast-paced ecosystem.

Navigating the Global Supply Chains of the Semiconductor Industry

The semiconductor device industry relies heavily on global ecosystems, making supply chain resilience and risk mitigation crucial for sustained success. Recent disruptions and geopolitical tensions have highlighted the vulnerabilities of the semiconductor supply chain.

The semiconductor industry is geographically concentrated in a few places, primarily the U.S., Taiwan, Korea, Japan, Europe, and mainland China. The dominance of U.S.-based semiconductor device companies is historical; in the last five years, they have maintained a 53% market share. If we combine all types of semiconductor company business models, i.e., adding the open foundries, OSAT, equipment, and material companies, the market share of U.S. companies drops to 41%; if only the added value is considered, then the U.S. share becomes 32%, and this number has been diminishing at a rate of 1 percentage point per year in the last five years.

U.S. semiconductor companies have developed the fabless business model, which helped maintain their dominance but created huge vulnerabilities toward Taiwan.

Advancing Semiconductor Technologies are Shaping the Semiconductor Landscape

The technology trend is no longer single-threaded. At the center of competition is the More Moore node race in the manufacturing process, currently 7 nm, 5 nm, and 3 nm, as well as future smaller nodes. These cutting-edge processes allow for higher transistor density, improved performance, and energy efficiency though they pose significant challenges in terms of development costs, yield rates, and manufacturing complexity. The industry is, therefore, actively exploring innovative solutions through More than Moore approaches. NAND memory is headed full steam into 3D stacking, while advanced packaging has become vital for all leading players. Many innovations trends are driving the semiconductor industry; wide bandgap compound semiconductors, photonic integration, quantum computing, and neuromorphics will play their role in expanding the industry to serve a growing diversity of semiconductor device types.